The Fund delivered +0.68% in February (noting the 28 day month, this is equivalent to 0.75% for a 31 day month), 9.61% over 12 months and 8.95% annualised over three years continuing to deliver over 5% net return above the RBA cash rate.

Examining Australian Credit Markets

A rise in recent volatility has disrupted the longer-term theme of decreasing credit spreads, which historically has seen longer-term-to-maturity assets outperform short-dated equivalents, a trend we see likely reversing. Our investment thesis centres on buying short-dated assets, meaning a rise in volatility is welcomed. Increased volatility has the potential to increase the yield we can demand on a given security, while our existing portfolio value is only marginally impacted by these new yields. Opposingly, a fund buying longer dated assets will have less ability to ‘reset’ their portfolio into higher-yielding assets since capital isn't paid back as quickly and their current portfolio falling in value given the mark to market exposure.

At a time when equities have generally fallen in value, longer-dated assets have offered limited portfolio diversification. While it is too early to postulate if this rise in volatility is a point-in-time dynamic or if we are entering a new market dynamic, we anticipate a more material divergence in our Fund's performance vs peers that, in general, are more exposed to longer-dated assets.

New Investor Reporting

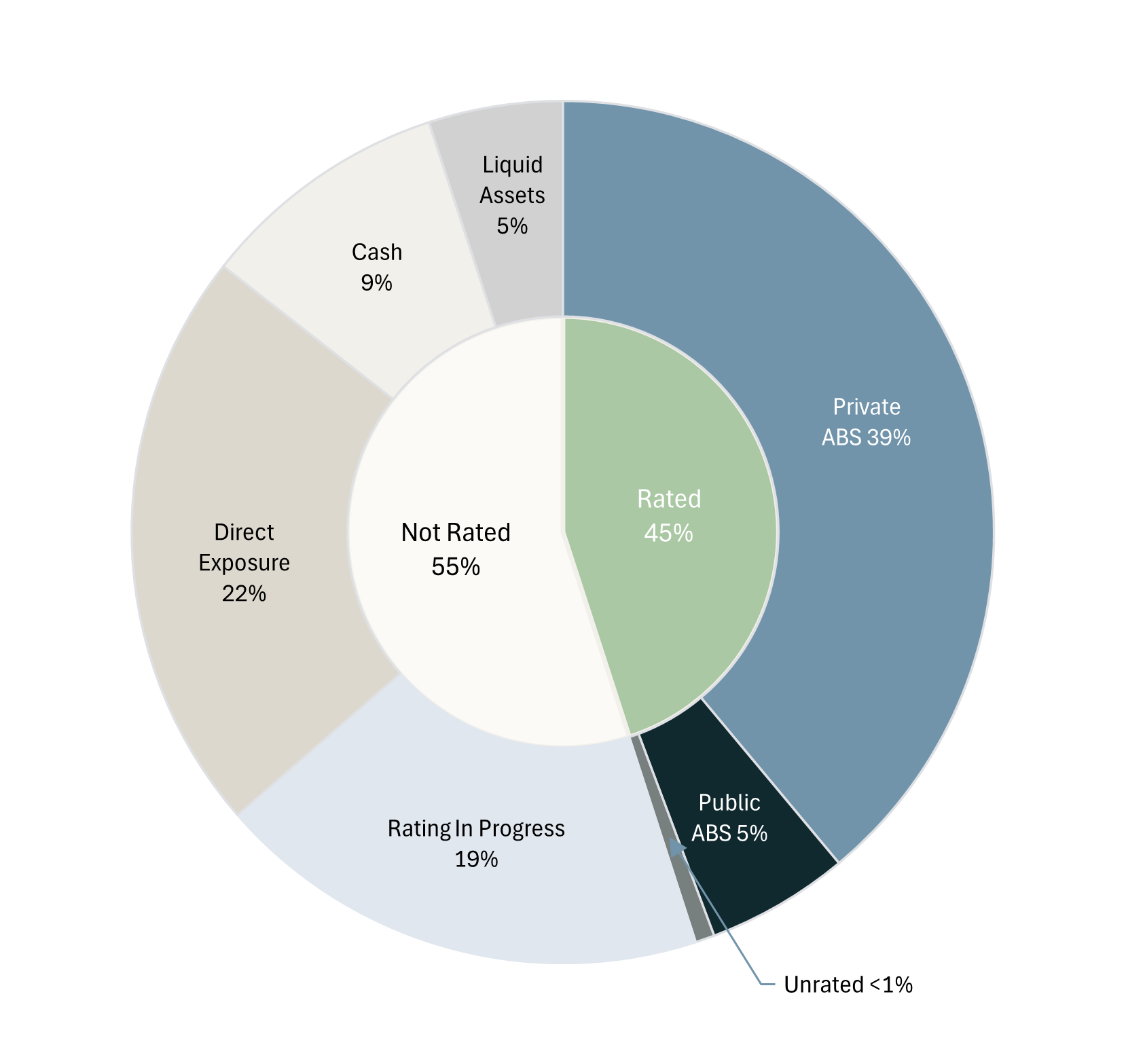

Following a 12-month process, we are pleased to release our enhanced investor reporting disclosure, as seen below, including a large portion of the portfolio being credit rated by an independent third party. We are pleased to provide this at a time when investor disclosure is paramount using industry best practice standards.

Portfolio Composition**

Credit Quality**

Portfolio Composition:

- Private ABS: refers to assets directly negotiated and held by the fund. The indicative credit rating shown is based on ratings data provided by an independent third party.

- Public ABS: refers to publicly rated securities issued on the market and purchased by the fund. The credit rating shown is based on the public rating provided by S&P or Moody’s.

- Rating in progress: these are Private ABS securities with an indicative credit rating in progress with a target release date of July 2025.

- Direct: individual, senior first mortgages held by the Fund

The portfolio composition chart will be updated monthly with the credit quality and corresponding chart being reassessed quarterly using updated data. We look forward to a growing prevalence of funds disclosing portfolio holdings within the industry and are proud to play our role in that evolution.